Freshers

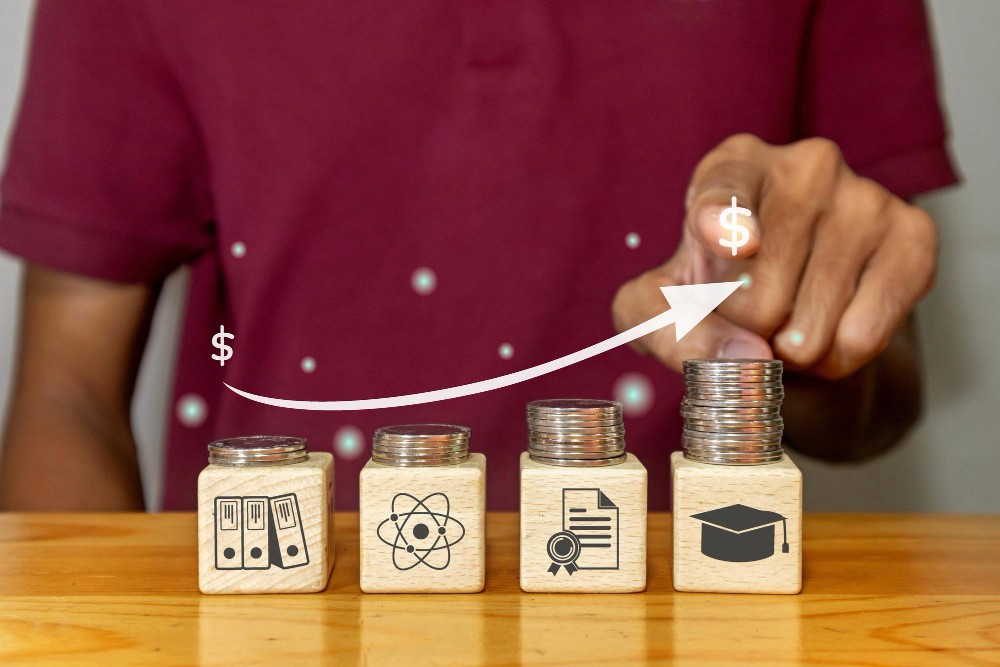

Navigating Financial Challenges as a New Graduate: Smart Strategies for a Stable Start

Team NxtClue

|

7 mins

|

Sep 1, 2024

0:00/1:34

Don't have enough time to read?

Listen

Navigating Financial Constraints as a Fresher: Smart Strategies for a Smooth Start

Picture this: You’ve just stepped out of college, diploma in hand, and you’re ready to conquer the professional world. The excitement of securing your first job is palpable, but reality soon hits. The starting salary isn’t quite what you hoped for, student loan payments loom large, and the costs of relocating to a new city are daunting. Suddenly, the thrill of beginning your career is overshadowed by financial stress.

If this sounds like you, you’re not alone. Many fresh graduates face similar financial challenges when entering the job market. The good news is that there are ways to navigate this initial phase strategically and set yourself up for financial stability and growth. Let’s explore some practical strategies to help you manage your finances effectively as you embark on your professional journey.

Does This Sound Like You?

Meet Rohan. He recently graduated with a degree in Engineering and landed his first job in a big city. Excited to start, he soon realized that his salary barely covers his rent, student loan payments, and daily expenses. He’s frustrated and worried about making ends meet, let alone saving for the future. Rohan’s story is all too familiar for many freshers who feel the pressure of financial constraints as they start their careers.

If you’re nodding along, don’t worry—you’re not alone. Financial planning as a fresher can be challenging, but with the right approach, you can overcome these hurdles and build a solid foundation for your future.

1. Create a Realistic Budget and Stick to It

The first step to managing your finances is to create a realistic budget that accounts for all your income and expenses. List down your essential expenses—like rent, utilities, transportation, groceries, and student loan payments—and compare them against your monthly income. Identify areas where you can cut back or save.

Tip:

“Use budgeting apps like Mint or YNAB (You Need A Budget) to help you track your expenses and maintain discipline. Set spending limits and stick to them to avoid unnecessary expenses.”

2. Prioritize Paying Off High-Interest Debt

Student loans are often the biggest financial burden for freshers. If you have multiple loans, prioritize paying off those with the highest interest rates first. This strategy, known as the “avalanche method,” helps you save money on interest over time.

Tip:

“Consider consolidating your loans or refinancing to get a lower interest rate. Research different repayment plans and choose one that aligns with your financial situation and career goals.”

3. Build an Emergency Fund

An emergency fund is a financial safety net that helps you cover unexpected expenses, such as medical bills or car repairs. Aim to save at least three to six months’ worth of living expenses in a separate savings account. Start small if you need to, but make it a priority to contribute regularly.

Tip:

“Set up an automatic transfer to your emergency fund each month, even if it’s just a small amount. Consistent contributions add up over time and help build a cushion for unexpected events.”

4. Consider Cost-Effective Living Arrangements

Relocating to a new city can be expensive, especially if it involves high rent costs. Consider more cost-effective living arrangements to ease your financial burden. Sharing an apartment with roommates, living with family temporarily, or finding housing close to work to save on transportation can all be viable options.

Tip:

“Look for housing options that offer utilities included in rent, or consider subletting or temporary housing while you get a feel for the city. This can help you avoid long-term financial commitments until you’re more financially secure.”

5. Explore Additional Income Streams

Consider taking on a part-time job or freelance work to supplement your income. Many freshers find success in freelancing or gig work, which not only provides extra cash but also enhances skills and builds a network that can be beneficial for career growth.

Tip:

“Platforms like Upwork, Fiverr, or even local part-time opportunities can provide flexible work options that fit around your primary job. Look for gigs related to your field to gain experience while earning extra income.”

6. Take Advantage of Employer Benefits and Discounts

Many companies offer benefits and discounts that can help you save money. These can include health insurance, travel discounts, or even subsidized meals. Make sure you’re fully aware of all the benefits available to you and take advantage of them wherever possible.

Tip:

“Speak with your HR department to understand the full range of benefits offered by your employer. Small savings on things like transportation or meals can add up significantly over time.”

7. Start Investing Early, Even with Small Amounts

While it may seem daunting to start investing with a limited income, beginning early has its advantages due to the power of compounding. Even small, regular investments in a low-cost index fund or mutual fund can grow significantly over time.

Tip:

“Consider using micro-investing apps like Acorns or Stash, which allow you to invest spare change or small amounts. Over time, this can grow into a substantial investment portfolio.”

8. Educate Yourself on Personal Finance

Knowledge is power, especially when it comes to managing your finances. Invest time in learning about personal finance, budgeting, saving, and investing. There are plenty of free resources available online, from blogs and podcasts to online courses.

Tip:

“Follow personal finance influencers and educators on social media platforms like Instagram or Twitter for daily tips and advice. Books like ‘Rich Dad Poor Dad’ by Robert Kiyosaki or ‘The Simple Path to Wealth’ by JL Collins can also provide valuable insights.”

Wrapping Up

Navigating financial constraints as a fresher can be challenging, but it’s entirely manageable with the right strategies and mindset. By creating a budget, prioritizing debt repayment, building an emergency fund, considering cost-effective living arrangements, exploring additional income streams, taking advantage of employer benefits, starting to invest early, and educating yourself on personal finance, you can overcome these initial hurdles and set yourself up for a financially stable future.

Ready to take control of your finances? Start implementing these strategies today, and remember—every small step you take now can lead to significant financial stability and growth in the future!

Navigating Financial Constraints as a Fresher: Smart Strategies for a Smooth Start

Picture this: You’ve just stepped out of college, diploma in hand, and you’re ready to conquer the professional world. The excitement of securing your first job is palpable, but reality soon hits. The starting salary isn’t quite what you hoped for, student loan payments loom large, and the costs of relocating to a new city are daunting. Suddenly, the thrill of beginning your career is overshadowed by financial stress.

If this sounds like you, you’re not alone. Many fresh graduates face similar financial challenges when entering the job market. The good news is that there are ways to navigate this initial phase strategically and set yourself up for financial stability and growth. Let’s explore some practical strategies to help you manage your finances effectively as you embark on your professional journey.

Does This Sound Like You?

Meet Rohan. He recently graduated with a degree in Engineering and landed his first job in a big city. Excited to start, he soon realized that his salary barely covers his rent, student loan payments, and daily expenses. He’s frustrated and worried about making ends meet, let alone saving for the future. Rohan’s story is all too familiar for many freshers who feel the pressure of financial constraints as they start their careers.

If you’re nodding along, don’t worry—you’re not alone. Financial planning as a fresher can be challenging, but with the right approach, you can overcome these hurdles and build a solid foundation for your future.

1. Create a Realistic Budget and Stick to It

The first step to managing your finances is to create a realistic budget that accounts for all your income and expenses. List down your essential expenses—like rent, utilities, transportation, groceries, and student loan payments—and compare them against your monthly income. Identify areas where you can cut back or save.

Tip:

“Use budgeting apps like Mint or YNAB (You Need A Budget) to help you track your expenses and maintain discipline. Set spending limits and stick to them to avoid unnecessary expenses.”

2. Prioritize Paying Off High-Interest Debt

Student loans are often the biggest financial burden for freshers. If you have multiple loans, prioritize paying off those with the highest interest rates first. This strategy, known as the “avalanche method,” helps you save money on interest over time.

Tip:

“Consider consolidating your loans or refinancing to get a lower interest rate. Research different repayment plans and choose one that aligns with your financial situation and career goals.”

3. Build an Emergency Fund

An emergency fund is a financial safety net that helps you cover unexpected expenses, such as medical bills or car repairs. Aim to save at least three to six months’ worth of living expenses in a separate savings account. Start small if you need to, but make it a priority to contribute regularly.

Tip:

“Set up an automatic transfer to your emergency fund each month, even if it’s just a small amount. Consistent contributions add up over time and help build a cushion for unexpected events.”

4. Consider Cost-Effective Living Arrangements

Relocating to a new city can be expensive, especially if it involves high rent costs. Consider more cost-effective living arrangements to ease your financial burden. Sharing an apartment with roommates, living with family temporarily, or finding housing close to work to save on transportation can all be viable options.

Tip:

“Look for housing options that offer utilities included in rent, or consider subletting or temporary housing while you get a feel for the city. This can help you avoid long-term financial commitments until you’re more financially secure.”

5. Explore Additional Income Streams

Consider taking on a part-time job or freelance work to supplement your income. Many freshers find success in freelancing or gig work, which not only provides extra cash but also enhances skills and builds a network that can be beneficial for career growth.

Tip:

“Platforms like Upwork, Fiverr, or even local part-time opportunities can provide flexible work options that fit around your primary job. Look for gigs related to your field to gain experience while earning extra income.”

6. Take Advantage of Employer Benefits and Discounts

Many companies offer benefits and discounts that can help you save money. These can include health insurance, travel discounts, or even subsidized meals. Make sure you’re fully aware of all the benefits available to you and take advantage of them wherever possible.

Tip:

“Speak with your HR department to understand the full range of benefits offered by your employer. Small savings on things like transportation or meals can add up significantly over time.”

7. Start Investing Early, Even with Small Amounts

While it may seem daunting to start investing with a limited income, beginning early has its advantages due to the power of compounding. Even small, regular investments in a low-cost index fund or mutual fund can grow significantly over time.

Tip:

“Consider using micro-investing apps like Acorns or Stash, which allow you to invest spare change or small amounts. Over time, this can grow into a substantial investment portfolio.”

8. Educate Yourself on Personal Finance

Knowledge is power, especially when it comes to managing your finances. Invest time in learning about personal finance, budgeting, saving, and investing. There are plenty of free resources available online, from blogs and podcasts to online courses.

Tip:

“Follow personal finance influencers and educators on social media platforms like Instagram or Twitter for daily tips and advice. Books like ‘Rich Dad Poor Dad’ by Robert Kiyosaki or ‘The Simple Path to Wealth’ by JL Collins can also provide valuable insights.”

Wrapping Up

Navigating financial constraints as a fresher can be challenging, but it’s entirely manageable with the right strategies and mindset. By creating a budget, prioritizing debt repayment, building an emergency fund, considering cost-effective living arrangements, exploring additional income streams, taking advantage of employer benefits, starting to invest early, and educating yourself on personal finance, you can overcome these initial hurdles and set yourself up for a financially stable future.

Ready to take control of your finances? Start implementing these strategies today, and remember—every small step you take now can lead to significant financial stability and growth in the future!

0:00/1:34

Don't have enough time to read?

Listen

7 mins

Freshers

Navigating Financial Challenges as a New Graduate: Smart Strategies for a Stable Start

Team NxtClue

|

Sep 1, 2024

Copyright © 2024 NxtClue | All Rights Reserved

I May Not Be the Menu, But I Can Still Guide You – I Know Some Shortcuts!

With us

Decision is yours

Without us

Copyright © 2024 NxtClue | All Rights Reserved

I May Not Be the Menu, But I Can Still Guide You – I Know Some Shortcuts!

With us

Decision is yours

Without us

Related Blogs

Related Blogs

I May Not Be the Menu, But I Can Still Guide You – I Know Some Shortcuts!

With us

Decision is yours

Without us

Copyright © 2024 NxtClue | All Rights Reserved